The era of isolated autonomy is ending. The real opportunity lies in the system beneath it.

When Waymo’s driverless cars began logging rides across San Francisco and Phoenix, the world collectively marveled at the vehicle. The sensor suite, the neural network, the billion-dollar training data. And rightly so — it was remarkable. But as someone who has spent the better part of two decades looking at where durable value actually accumulates in technology transitions, I keep returning to a different question: what happens when every city has a fleet of autonomous vehicles, and none of them can talk to each other, to the traffic grid, or to the drone delivering your package three meters overhead?

That question is the thesis. We are leaving Autonomy 1.0 — single-system, geofenced, isolated deployments — and entering Autonomy 2.0: orchestrated, integrated, community-embedded autonomous systems. The locus of value creation is shifting from the vehicle to the coordination layer that connects everything. At Opulentia, this is exactly the kind of structural inflection point we build theses around.

From Pilots to Platforms: The Numbers Are No Longer Theoretical

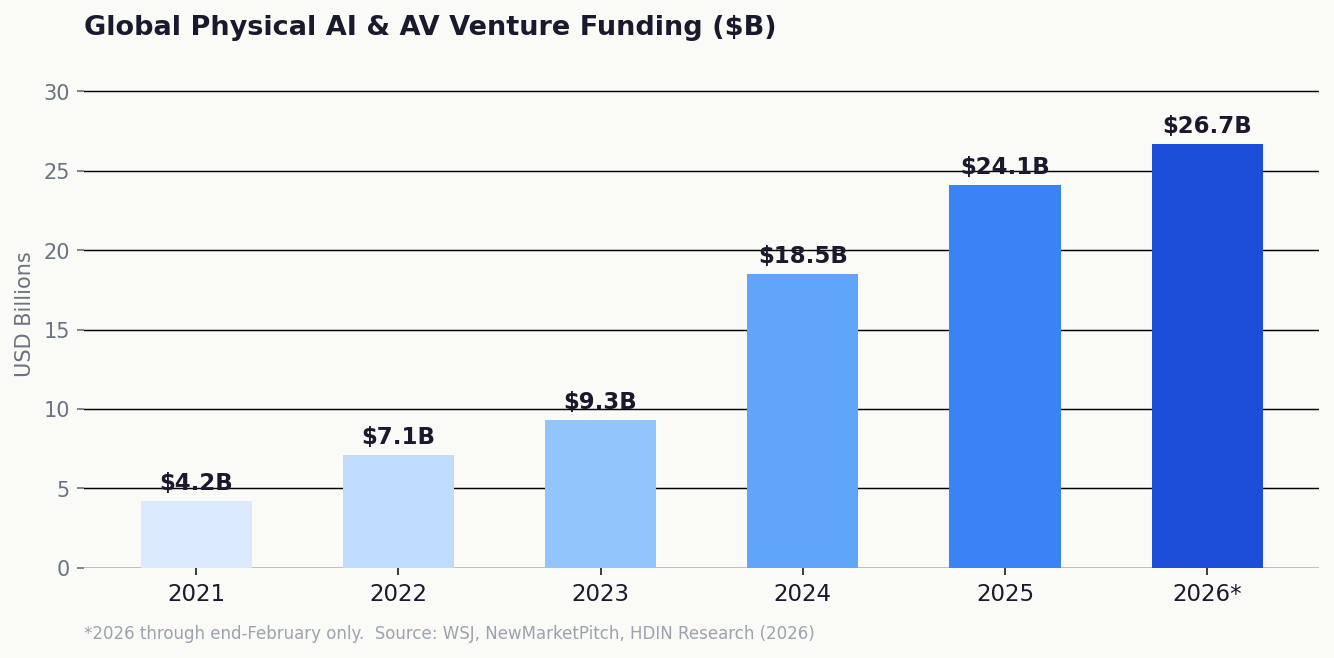

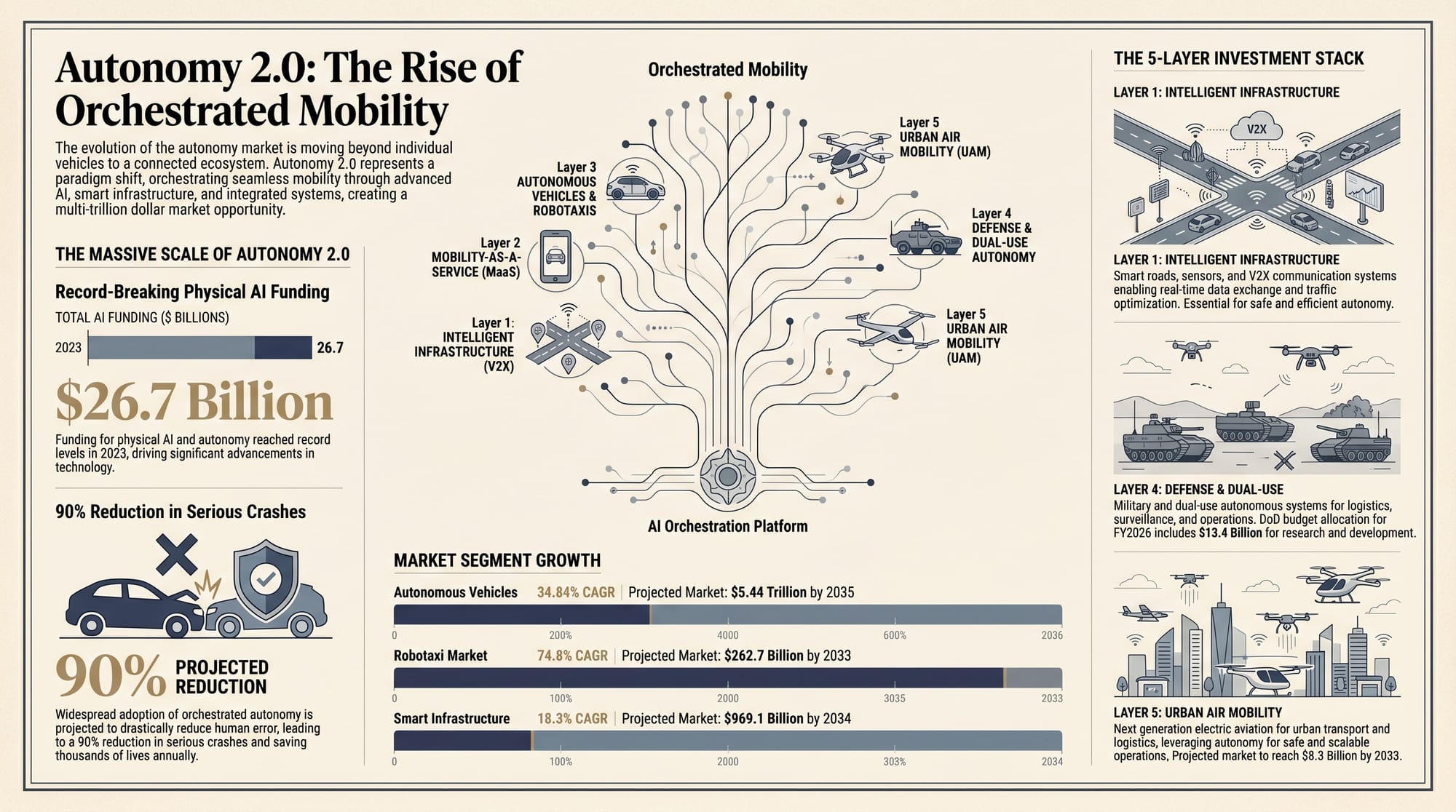

Cumulative Level 5 driverless mileage crossed 536 million miles as of March 2026 — a milestone that Stifel Institutional used to anchor its own ‘Autonomy 2.0’ research report, calling it the ‘commercial inflection’ moment for the industry. Physical AI venture funding reached $26.7 billion globally by the end of February 2026 alone, already surpassing every prior annual total. The robotaxi sector has absorbed more than $50 billion in aggregate investment across 2025–2026.

Figure 1: Global Physical AI & AV Venture Funding, 2021–2026

These are not speculative projections. The World Economic Forum’s 2026 briefing on Next-Generation Physical Autonomy maps four concrete scenarios for autonomous systems by 2031, noting that AI will ‘increasingly live in machines that can sense, move, manipulate, and collaborate in the physical world.’ PwC’s autonomous mobility report concluded the industry has definitively transitioned from ‘pilot to implementation.’ The policy environment is crystallizing in parallel: the SELF DRIVE Act of 2026 (H.R. 7390), introduced in February, creates the first federal framework for autonomous driving system deployment and gives NHTSA the authority the industry has needed since Waymo’s earliest pilots.

The Five Layers of the Autonomy 2.0 Investment Thesis

The market opportunity is not one story — it is five compounding layers, each with distinct risk/return profiles and entry points.

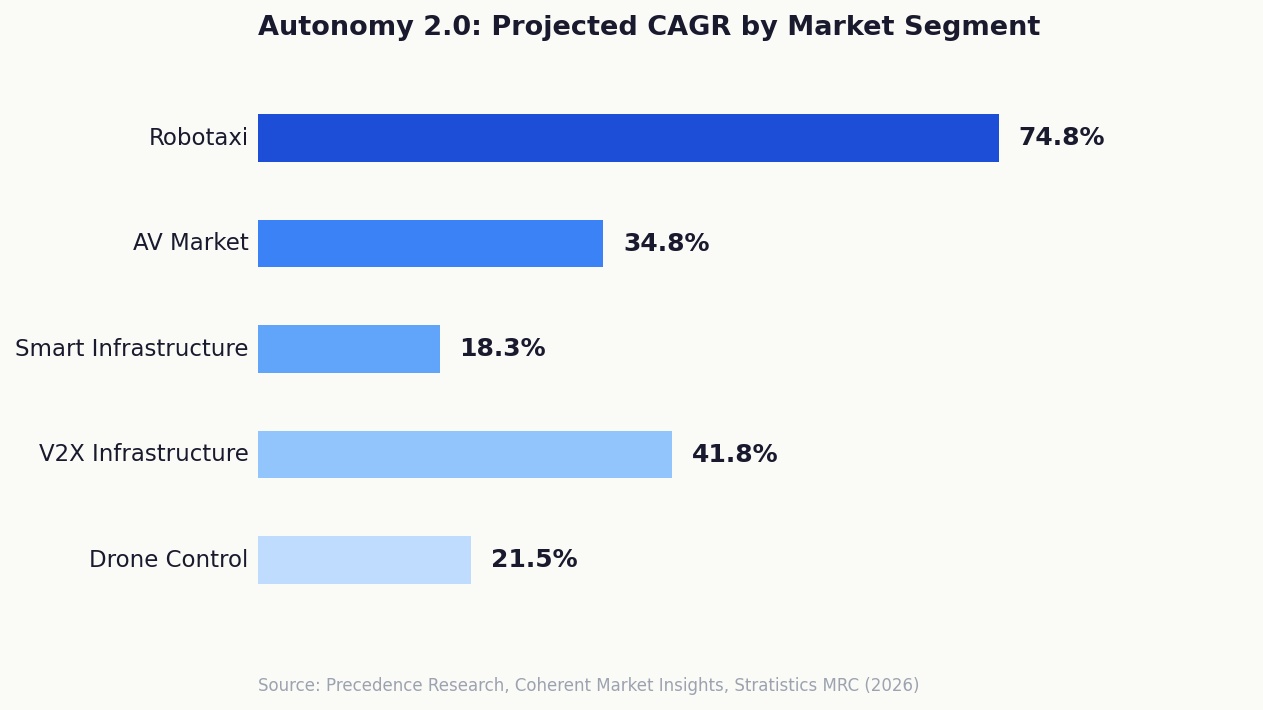

Figure 2: Projected CAGR by Autonomy 2.0 Market Segment

The Numbers Are Not Small

Before examining the investment layers, it is worth anchoring the scale. The global autonomous vehicle market, valued at $273.75 billion in 2025, is projected to reach $5.44 trillion by 2035 at a CAGR of 34.84% (Precedence Research). The robotaxi segment alone is growing at 74.8% CAGR with projections reaching $262.7 billion by 2033 (Coherent Market Insights). Smart infrastructure is projected to reach $969 billion by 2034. Vehicle-to-everything (V2X) communications — the technical backbone of orchestration — is projected to grow from under $4 billion today to $29 billion by 2035 (Research and Markets).

Layer 1 — Intelligent Infrastructure (The Underinvested Bet)

The V2X market is growing at 41.8% CAGR toward $22.3 billion by 2034, within a broader smart infrastructure market on course for $969 billion. This is where I see the most durable, least crowded opportunity — foundational rails that every autonomous system will depend on.

Layer 2 — Robotaxi & Physical AI Deployment

The robotaxi market is projected at 74.8% CAGR, reaching $262.7 billion by 2033. Waymo raised $16 billion in early 2026; Tesla’s Cybercab entered production in April 2026 with projected fares as low as $0.20/mile. The early-stage vehicle-level window is largely closed — the accessible plays are mid-stack: fleet orchestration, edge AI, and training data infrastructure (Uber’s AV Labs alone is generating over three million hours of training data).

Layer 3 — Enterprise Orchestration (The Cross-Sector Pattern)

Andreessen Horowitz named enterprise orchestration a defining Big Idea for 2026 — the shift from isolated AI copilots to coordinated multi-agent systems. Deloitte projects the autonomous AI agent market at $8.5 billion by 2026, scaling to $35 billion by 2030. The architectural insight: companies positioned as coordination layers in logistics, defense, or mobility share a common structural moat.

Layer 4 — Defense & Dual-Use Autonomy

The 2026 NDAA — the largest military budget in American history — includes substantial funding for AI-enabled autonomous systems. The proposed Intelligent Infrastructure Commerce and Defense Act frames this infrastructure explicitly as the “nervous system of the American economy.” The convergence of civil and defense autonomy creates a dual-use corridor that aligns directly with Opulentia’s existing defense tech positioning.

Layer 5 — Urban Air Mobility

Joby Aviation advanced toward FAA certification in late 2025. The autonomous drone traffic control market is projected to grow from $0.75 billion today to $8.3 billion by 2033. eVTOL and autonomous cargo drones represent the vertical dimension of Autonomy 2.0 — and managing low-altitude urban airspace alongside ground-based fleets is precisely the integrated orchestration challenge this thesis addresses.

The Bear Case We Take Seriously

A credible investment thesis must confront its own risks. Four concerns warrant genuine attention. First, capital concentration: the top three AV deals captured 53% of all 2025 funding, and early-stage seed capital has largely dried up — mid-market selection becomes critical. Second, unit economics: Waymo’s ‘Other Bets’ reported a $7.5 billion operating loss despite market leadership; gross margins require scale that most markets have not reached. Third, regulatory fragmentation: despite progress under the SELF DRIVE Act, the US still operates under a patchwork of state-level rules. Fourth, infrastructure lag: the orchestration thesis only pays off if the infrastructure layer scales in tandem with the vehicle layer — and history shows infrastructure routinely trails the technology it is built to support.

Why We Are Watching This Closely

Most commentary on autonomous vehicles focuses on technology milestones or company profiles. The Autonomy 2.0 framing differs in that it shifts the unit of analysis from the vehicle to the system — specifically, to the coordination layer that makes the system more than the sum of its parts. This is where infrastructure investors, defense allocators, and physical AI funds converge. It is a rare configuration.

“The real money in every technology transition is made not by those who build the train, but by those who lay the track.”

At Opulentia, we are actively evaluating opportunities across the intelligent infrastructure and defense dual-use corridors — the two layers we assess as most contrarian and most defensible given current market pricing. If you are building in this space or an LP curious about how we think about physical AI allocation, we want to have that conversation.

About Opulentia Ventures

Opulentia Ventures operates as a “VC Tribe” consolidating resources from experienced investors to support pioneering companies focused on technological advancements, healthcare, and national security. Headquartered in the Washington, DC, metro area, the firm leverages deep government and defense-sector relationships to identify emerging opportunities at the intersection of innovation and national priorities.

Media Contact:

Opulentia Ventures

info (at) opulentia (dot) vc

12901 Worldgate Drive,

Suite 600

Herndon, VA 20170