Every ambitious deep‑tech founder eventually asks the same forbidden question:

“How do we sell to the U.S. government? We’ve heard they have deep pockets — and they’re the biggest buyer in the world.”

On the surface, they’re right; the US federal government is the single largest purchaser of goods and services on the planet.

Underneath, what they’re really wrestling with is dual-use: “How do we take a product that wins in the commercial world and also make it work for defense, national security, and civilian federal agencies?” That’s where the fairy tale collapses. Behind those “deep pockets” is a procurement machine the White House itself has described as “prohibitively inefficient and costly,” plus layers of security, accreditation, and mission‑specific requirements that turn the federal valley of death into something far deeper than most commercial founders have ever seen.

"It's what insiders call the 'lab-to-field' problem — the chasm between a technology that works in controlled conditions and one that works where it matters."

Over the last decade, there have been serious attempts to fix this. The Defense Innovation Unit (DIU) — whose origin story is brilliantly chronicled in the book UnitX (read my previous review of the book here)— was created precisely to bridge Silicon Valley and the Pentagon, experimenting with faster pathways, commercial-style contracting, and on‑ramps for startups. DIU, AFWERX, NavalX, and others have shown it’s possible to get commercial tools into government hands faster, even if the broader system is still catching up.

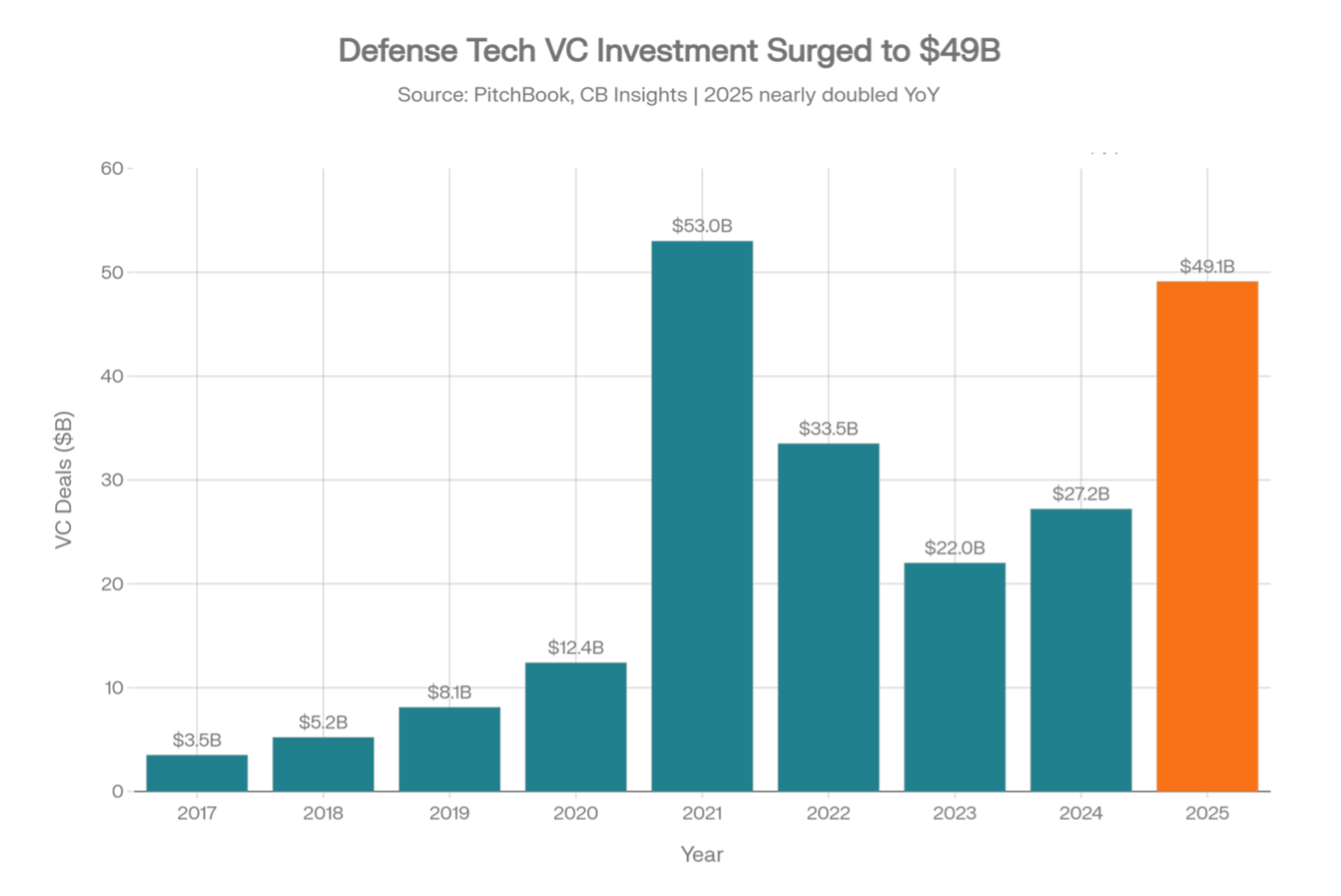

Meanwhile, the macro picture is on fire. Venture capital investment in defense and dual-use tech hit roughly $49.1 billion in 2025, up from about $27.2 billion the year before. One in four tech scaleups across NATO countries now qualifies as dual-use, with total investment around $1.2 trillion.

So the question isn’t “Is dual-use worth it?” It’s: Can your company actually become dual-use ready — across technology, funding, and customers — before you run out of time or identity?

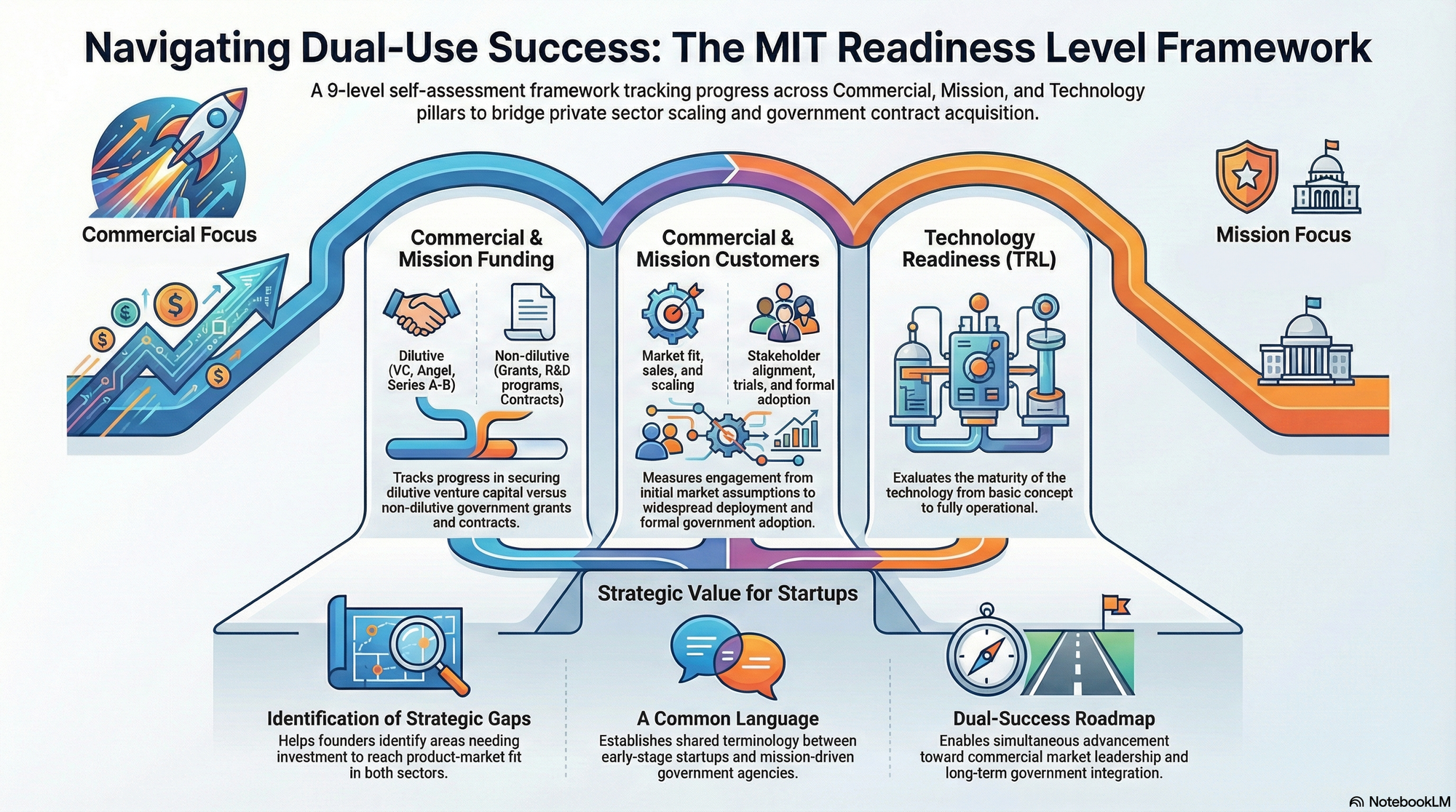

A recent readiness framework out of MIT helped me crystallize what I’d been seeing in the field for years: dual-use isn’t a single score, it’s a five‑dimensional profile. What follows is a field guide to those dimensions and the surprising truths that emerge from them.

Technology Readiness Is the Least Important Dimension You’re Ignoring

Every deep‑tech founder knows their Technology Readiness Level (TRL). It’s the classic 1–9 scale: basic principles at TRL 1, fully proven and operational systems at TRL 9. Useful, but deeply incomplete.

The dual-use readiness model extends this into five axes, each with nine levels:

- TRL – Technology Readiness

- CFRL – Commercial Funding Readiness

- CCRL – Commercial Customer Readiness

- MFRL – Mission Funding Readiness

- MCRL – Mission Customer Readiness

You can be TRL 7 (validated in an operational environment), yet sit at MFRL 2 (you’ve only identified possible grants) and MCRL 1 (mission stakeholders barely know you exist). On paper, the tech is “ready”; in reality, the system has nowhere to plug it in.

Dual-use insight: maturity isn’t one‑dimensional. A “ready” technology with immature funding and customer readiness is functionally not ready.

There Are Two Completely Different Funding Games — and You Must Play Both

Most founders know the commercial funding ladder by heart:

Angels / pre‑seed → Seed → Series A/B → growth / strategic → exit

That path is what the framework calls CFRL — from CFRL 1 (“exploring bootstrapping and pre‑seed”) to CFRL 9 (“scaling, market expansion, and strategic investments with a focus on exit”).

But dual-use demands a parallel ladder: MFRL, the mission funding path.

- Early (MFRL 1–3): exploring dual-use strategy, mapping mission use cases, identifying and applying to SBIR/STTR and other programs

- Middle (MFRL 4–6): winning first non‑dilutive awards, aligning with mission partners, applying for follow‑on phases

- Late (MFRL 7–9): substantial investment from procurement partners, enduring pathways into production, and integration into mission budgets

The clocks are wildly different. A commercial round can close in weeks or months; an SBIR Phase I or II can take 6–12 months to award, with additional years before you see a production contract.

The founders who win at dual-use:

- Use CFRL to buy time and build a product

- Use MFRL to prove mission value and de‑risk adoption

- Intentionally model cash around both timelines instead of hoping one magically covers the other

The “Valley of Death” Is Real — and Deeper on the Federal Side

In startup land, the valley of death is the gap between initial traction and a sustainable business. In defense, it’s the gap between “promising prototype” and “program of record.”

Studies and industry analysis paint a harsh picture:

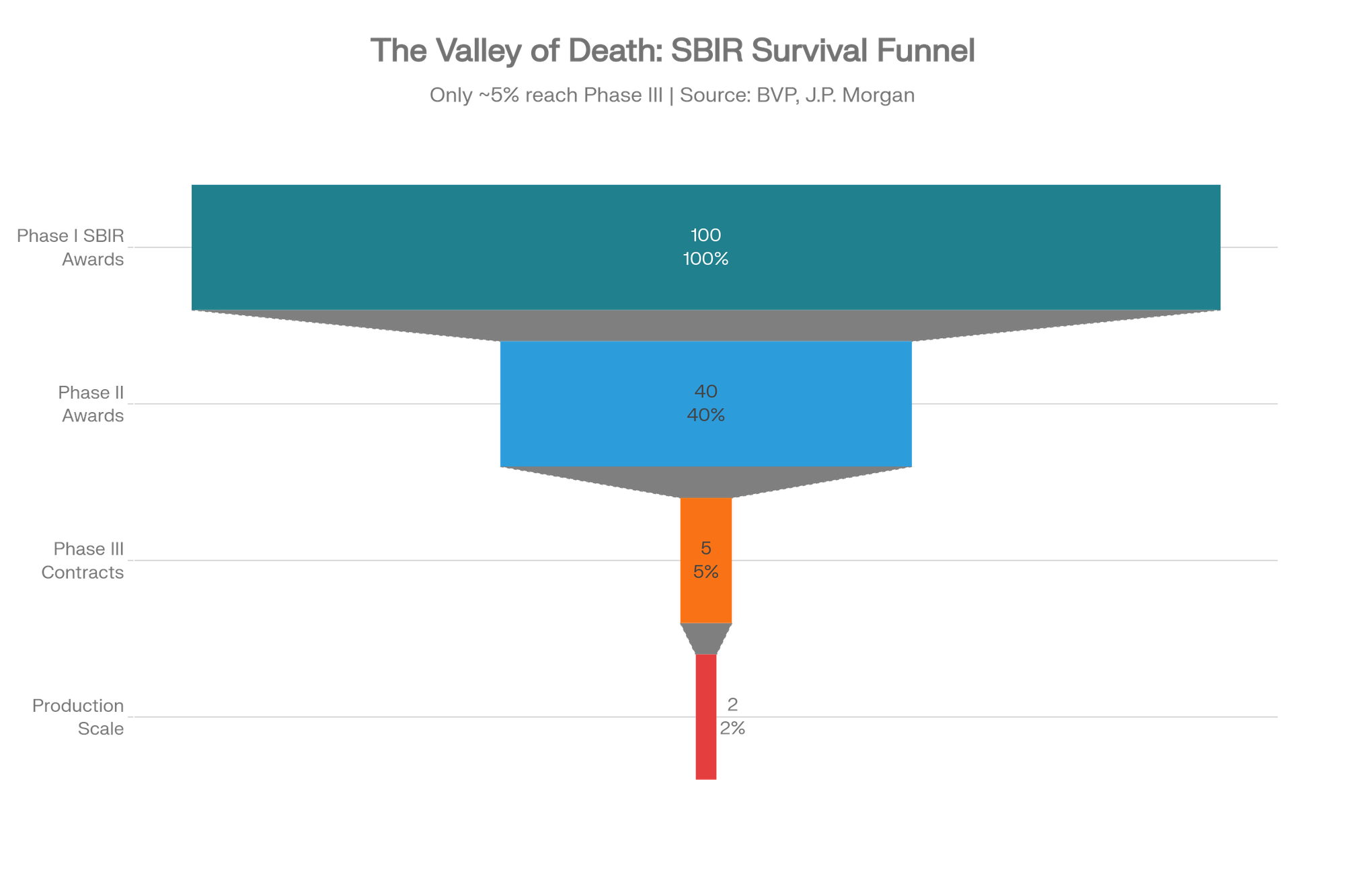

- Only about 16%-18% of DoD SBIR‑funded companies have historically reached a Phase III contract.

- Some estimates put the Phase II → Phase III graduation rate at roughly 5%.

One DoD program manager described it as a literal gap at the end of the bridge — startups cross years of development and testing only to hear, “We love it, come back in two years when the budget catches up.”

Here’s the nuance, though: SBIR/STTR isn’t fool’s gold. Long‑term studies show many Phase II projects go on to generate sales, increase employment, attract private capital, and even become acquisition targets. I know founders who are quietly building large, durable companies on a foundation of SBIR/STTR and follow‑on mission work.

The difference? They use the money to climb the MFRL and MCRL ladders — toward procurement relationships and standard‑issue adoption — rather than cycling in place as perpetual grant‑takers.

Customer Readiness Is a Two‑Body Problem — and It’s Where Most Startups Spin Out

Funding is one thing; customers are another. The readiness model splits customer maturity into commercial (CCRL) and mission (MCRL) — and the contrast is instructive.

Commercial customer readiness (CCRL):

- Starts with broad market assumptions

- Narrows to specific requirements and beachhead segments

- Moves through pilots and initial sales

- Ends with scalable, repeatable product revenue (CCRL 9)

Mission customer readiness (MCRL):

- Starts with basic awareness among mission stakeholders

- Evolves through capability discussions, use‑case refinement, and experiments

- Requires letters of intent, formal evaluations, and validation in mission environments

- Ends with formal adoption into systems, training, or doctrine — and eventually standard‑issue deployment (MCRL 8–9)

You are essentially solving a two‑body problem:

- Two sets of buyers, with different incentives, vocabularies, and risks

- Two sales cycles — 12–24 months on the commercial side vs. often 3–7 years on the mission side

- Two proof stacks — case studies and ROI vs. mission impact, survivability, and doctrine

Trying to brute‑force both with one generic GTM motion is how you burn runway and team morale at the same time.

GPS Was Dual-Use by Design — and So Is Your Tech

We often tell the GPS story as “a military technology that was later opened up to civilians.” The architects themselves tell it differently: from the earliest days, GPS was conceived as a system with both military and civilian applications.

What changed over time wasn’t the underlying technology, but:

- Policy decisions after events like the KAL 007 tragedy

- Choices about signal accuracy and access

- Governance over how a dual-use infrastructure would be managed for decades

"GPS already had civilian signals; KAL 007 changed the political commitment to guarantee that access."

The lesson for today’s AI, autonomy, sensing, quantum, and cyber founders is clear: your technology is dual-use, whether you like it or not. The real choice is whether you design:

Architectures that can support both civilian and mission-grade requirements

- Product and deployment models that can handle classification, export controls, and safety regimes

- A company that can responsibly navigate the ethical and geopolitical implications

Dual-use isn’t a pivot; it’s a design philosophy.

The Biggest Risk Isn’t Tech Failure — It’s Identity Crisis

Look across the dual-use landscape, and you’ll see a familiar pattern: promising companies that are “too defense” for commercial buyers and “too commercial” for defense buyers. Analysts call it the “not here nor there” problem.

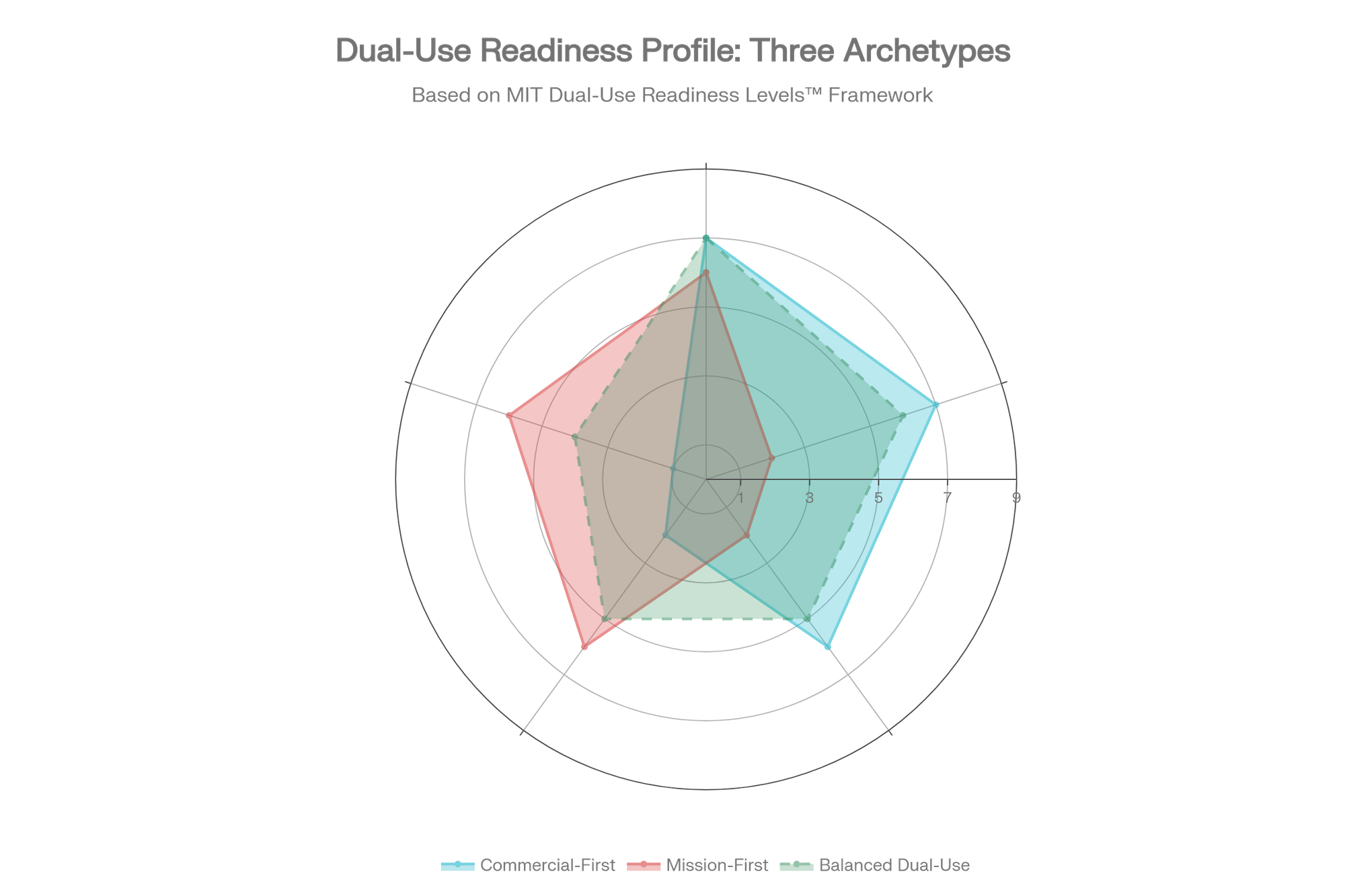

The five-axis profile makes that visible. Consider two extremes:

- Commercial-first: CFRL 7, CCRL 6, but MFRL 2, MCRL 1. This is a commercial company dabbling in dual-use branding.

- Mission-first: MFRL 6, MCRL 6, but CFRL 2, CCRL 2. This is a mission company with optional commercial upside.

Neither is wrong. The danger is pretending you’re a perfectly balanced dual-use platform when your actual scores say otherwise.

The companies that avoid identity crisis tend to:

- Explicitly choose a starting side: “We are commercial‑first with a deliberate mission thesis” or “mission‑first with targeted commercial wedges.”

- Staff both dialects: Pair people who understand CAC, LTV, and PLG with people who understand FAR, OTAs, and PPBE.

- Use the readiness levels as a mirror, not a vanity metric, to make strategy decisions.

We’re Entering the Production Era — and the Framework Needs Its Next Evolution

One more shift is underway: from the prototype era to the production era of defense tech.

2025 was the strongest funding year on record; equity funding for defense tech more than doubled year‑on‑year, and at least ten new military‑focused unicorns emerged. But investors and government stakeholders are now asking a new question: Can you actually build and support this at scale?

Manufacturing‑oriented defense deals nearly doubled to about $4.7 billion across +/- 39 deals in 2025, signaling a growing recognition that exquisite prototypes don’t win wars — mass‑producible, adaptable, replaceable systems do.

This suggests the current five‑axis readiness model is necessary but not sufficient. Once you’ve hit TRL 8–9, MFRL 8–9, and MCRL 8–9, the challenge becomes:

- Manufacturing readiness

- Supply chain and industrial base resilience

- Regulatory and export readiness (especially for NATO and allied markets)

In other words, a sixth and seventh axis are emerging — and the next generation of frameworks will need to capture them.

A Final Thought

Dual-use technology is no longer a niche corner of the ecosystem. It’s where some of the most important battles — technological, economic, and geopolitical — are being fought. But beneath the funding headlines and innovation theater, a quieter truth stands:

Dual-use is not just a feature of your product. It’s a capability of your organization.

It’s your ability to:

- Advance across technology, funding, and customer readiness — commercial and mission

- Navigate two funding cycles and two sales motions without losing your center

- Learn from experiments like DIU and the UnitX playbook, rather than reliving the pre‑DIU era of lock‑out and red tape

- And, increasingly, to turn prototypes into production at a scale that actually matters

So here’s the question I’d leave you with:

If you plotted your startup on a five‑axis radar chart tomorrow — technology, commercial funding, commercial customers, mission funding, mission customers — what shape would you see?

And if you were brutally honest, which axis would scare you the most?

This article draws extensively on, and is inspired by, the white paper “Introducing Dual-use Readiness Levels™: A Framework for Dual-use Strategy” by Keselman and Murray, developed at MIT. The Dual-use Readiness Levels™ framework, including its terminology, structure, and underlying research, is the sole work and intellectual property of the original authors and MIT. This article is provided solely as independent commentary and interpretation for informational purposes and does not create or imply any ownership interest, license, or other rights in that framework. Nothing herein should be construed as modifying, extending, or substituting for the authors’ original work.

My use of these ideas is limited to fair-use discussion, critique, and education; I do not claim, and expressly disclaim, any ownership, authorship, or proprietary interest in the Dual-use Readiness Levels™ framework or related materials.

About Opulentia Ventures

Opulentia Ventures operates as a “VC Tribe,” consolidating resources from experienced investors to support pioneering companies focused on technological advancements, healthcare, and national security. Headquartered in the Washington, DC, metro area, the firm leverages deep government and defense-sector relationships to identify emerging opportunities at the intersection of innovation and national priorities.