How a new class of autonomous engineering intelligence is quietly redefining what AI can do — and why it represents one of the most significant infrastructure-level investment opportunities of the decade.

The Central Thesis

The AI industry has spent the last five years perfecting intelligence capable of conversations. The next decade belongs to "intelligence that builds". We are at the earliest stages of a transition from AI systems that reason about the world to AI systems that operate within it — and the implications for capital allocation are profound.

The AGI Engineer is an autonomous intelligence system purpose-built to solve the hardest problems in the physical domain. Not to answer questions about engineering. Not to generate engineering documents. But to perceive, model, decide, act, and learn within real physical environments — bridging raw computational intelligence and the material world.

It is a thesis I have spent considerable time pressure-testing across defense primes, energy operators, semiconductor fabs, and aerospace OEMs. The data keeps pointing in the same direction. The shift is real and, in my view, irreversible. Project Prometheus is the effort I have been following most closely in this space — precisely because it is building at this exact intersection, and doing so with the seriousness the problem demands.

"The most valuable AI of the next decade will not live in a chat window. It will live on the factory floor, in the orbital design lab, and inside the reactor simulation stack."

The Architecture: A Closed-Loop Physical Intelligence

The loop below is not a metaphor — it is an architectural requirement. Without it, the system is advisory AI. It is an autonomous engineering agent.

The AGI Engineer Decision Loop

A closed-loop architecture that perceives physical reality, models it digitally, decides with multi-objective intelligence, acts on the world — and learns from every outcome.

Tap any node to explore each stage

A 30-Year Evolution

Four converging lineages built this moment:

From Drafting Tables to

Autonomous Physical Intelligence

Four decades of convergence — tap any era to explore the breakthrough that moved the needle.

Engineering moved from drafting tables to digital models. Tools like CATIA, AutoCAD, and ANSYS created the data layer that would eventually feed AI systems — a vast, structured repository of physical constraints, tolerances, and material behaviors.

Industrial giants connected physical assets to their digital representations. GE's Predix, Siemens' MindSphere, and NASA's twin-model methodology established continuous virtual-physical synchronization — the first closed loop between a real asset and its model.

Machine learning entered CAD optimization, predictive maintenance, and quality inspection. Each model solved one problem with extraordinary depth — but could not transfer intelligence across domains. A defect-detection model for turbine blades knew nothing about structural load analysis. Intelligence remained siloed.

Transformer architectures proved that massive pre-training yields generalizable reasoning. GPT-3, then GPT-4, DALL·E, and Codex demonstrated cross-domain transfer at scale. But these were still language and image models — powerful reasoning on tokens, not on physics. The open question crystallized: can this generalization extend to engineering constraints?

Multimodal models began ingesting sensor streams, CAD geometry, and simulation outputs. Physics-informed neural networks embedded governing equations directly into model architecture. Narrow AI began evolving toward domain Super-Intelligence — not general cognition, but domain-specific mastery exceeding human expert throughput. The question shifted: not "can AI reason?" but "can AI engineer?"

The AGI Engineer is not the next LLM. It is an autonomous intelligence system that perceives physical environments, constructs physics-accurate digital twins, makes multi-objective engineering decisions, and closes the loop with real-world outcomes. It operates across aerospace, defense, energy, semiconductors, and space — wherever the physical world demands precision at scale.

Why This Is Not Simply the Next GPT

The distinctions between the AGI Engineer and existing LLM platforms are architectural, economic, and strategic — and they matter enormously for how value accrues. Project Prometheus was conceived precisely at this boundary — not to build a better language model, but to build the first general-purpose reasoning system that speaks the language of physics.

LLM / Chat AI vs. AGI Engineer

This is not the next version of ChatGPT. The AGI Engineer operates in a fundamentally different problem space — click any row to understand why.

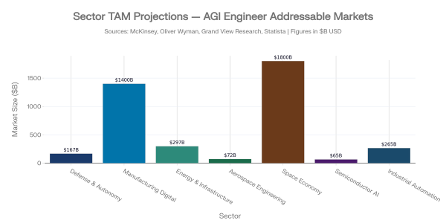

The Market Opportunity: $3.5 Trillion in Addressable Transformation

The TAM exceeds $3.5 trillion by the mid-2030s — built bottom-up from sector-specific forecasts validated by McKinsey Global Institute, Grand View Research, SNS Insider, Oliver Wyman, and L.E.K. Consulting. These are not AI hype numbers. They are engineering transformation numbers, each anchored in established capital expenditure cycles.

Sector Deep Dives

The AGI Engineer generalizes across every domain where engineering complexity, speed-to-certification, and operational reliability intersect. Below are the six highest-conviction verticals.

Defense & National Security: The U.S. Department of Defense allocated $13.4B in FY2026 for AI and autonomous systems — a figure that reflects existential urgency, not budgetary excess. The AGI Engineer addresses the DoD's most pressing capability gap: the ability to design, test, and field new systems at machine speed rather than acquisition-cycle speed.

The competitive moat in defense is not the model — it is the clearance, the certification stack, and the integration with existing C2 architecture. Players who can clear MIL-SPEC, IL5/IL6 cloud environments, and the CMMC framework hold a structural barrier that general-purpose LLM providers cannot replicate quickly.

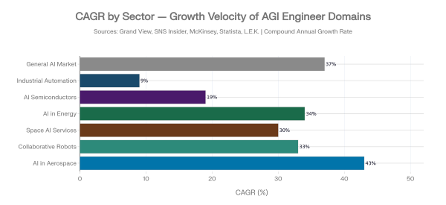

Aerospace Engineering: The AI in aerospace engineering market is projected to grow from $1.98B in 2023 to $71.76B by 2035 — a 43% CAGR. Structural loading, thermodynamics, avionics integration, and FAA/EASA certification pathways create a problem space precisely where AGI Engineering delivers the greatest time-to-certification compression.

Programs like NASA's Artemis, the USAF Next Generation Air Dominance initiative, and the commercial space expansion led by SpaceX and Blue Origin represent hundreds of billions in contracts that increasingly reward speed-to-specification over lowest-cost bids.

Smart Manufacturing & Industrial AI: The global smart manufacturing market is forecast to reach $1.4 trillion by 2030. The highest-value application is not robotic arm optimization — it is system-level design intelligence that redesigns production lines, reconfigures supply chains, and validates quality autonomously at speeds that eliminate human inspection bottlenecks.

The moat is the physical data flywheel: every hour an AGI Engineering system operates on a manufacturing floor generates proprietary sensor, quality, and performance data that continuously trains its physics model — compounding differentiation with every deployment.

Energy Infrastructure & Grid AI: The AI in the energy market is projected to reach $297B by 2035, driven by the decarbonization imperative and industrial electrification. Nuclear energy is a standout application: an AGI Engineer that autonomously runs neutronics simulations, thermal-hydraulic analysis, and regulatory compliance validation could compress the 10–15 year reactor licensing cycle by an order of magnitude.

Space Economy: The space AI services market is projected to reach $21.5B by 2035 at a 30% CAGR. Where every kilogram costs $2,000–$10,000 to orbit and failure is irretrievable, the AGI Engineer's physics-first optimization is uniquely valuable — and in-space manufacturing demands AI engineering systems that operate autonomously where human engineers cannot be present at all.

Semiconductors & Advanced Fabrication: VLSI chip design involves 15–20 billion transistors, thousands of design rules, and multi-week simulation cycles. AI-assisted EDA tools generated over $3.5B in revenue in 2024, growing at 19% CAGR. The AGI Engineer closes the loop between design simulation and fab process outcomes in real-time — dramatically reducing first-pass silicon failure rates and compressing time-to-tape-out.

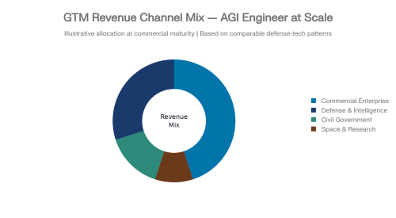

Three Routes to Market

The most durable businesses in this category will operate across all three channels simultaneously — using commercial deployments to fund the compliance investment required for government and defense.

Commercial Enterprise: Fortune 500 manufacturers, aerospace OEMs, and energy majors are the initial beachhead. Long evaluation cycles are offset by multi-year contracts and land-and-expand dynamics. The first deployment generates enough proprietary physical data to create a switching cost that grows nonlinearly over time.

Civil Government: AGI Engineering systems fit naturally with agencies managing nuclear, grid, space, and infrastructure programs — DOE, NASA, NIST, and the Army Corps of Engineers. Contract vehicles like OTAs and GSA Schedules provide accessible on-ramps for early-stage companies.

Defense & Intelligence: The highest ACV channel, requiring navigation of FedRAMP, ITAR/EAR, and CMMC in parallel with technical delivery. The reward: long-duration, sole-source

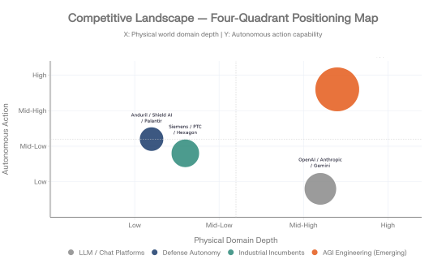

The Competitive Landscape

Four distinct clusters define the current field. Each has meaningful capabilities — and significant gaps that a purpose-built AGI Engineering platform can exploit.

LLM Platforms (OpenAI, Anthropic, Google DeepMind): Enormous model capability, zero physical domain depth. No physics simulation layer, no closed-loop feedback from physical systems, no credible pathway to FAA or MIL-SPEC certification. These players are partners and potential distribution channels — not direct competitors.

Defense Autonomy Players (Anduril, Shield AI, Palantir): Strong in autonomous decision-making for kinetic and surveillance operations. Their focus is the "act" phase — they do not address the full engineering lifecycle from design through deployment. Potential acquisition targets or strategic integration partners.

Industrial Software Incumbents (Siemens, PTC, Hexagon, ANSYS): Decades of domain knowledge in CAD, simulation, and PLM — but AI integration has been additive, not transformative. Their customer relationships are a channel opportunity, not a competitive threat, for a system that integrates with their platforms.

Point Solution AI Startups: A well-funded long tail addressing specific workflow nodes: generative design (nTopology), PCB layout (Celus), predictive maintenance (C3.ai). None has assembled the full closed-loop system. The category winner will likely emerge from this cohort.

Investment Signals: Green Flags and Red Flags

The checklist below separates genuine AGI Engineering platforms from sophisticated point solutions — designed for IC memos and initial diligence screens.

What to Look For in an AGI Engineering Investment

Seven signals separate category-defining platforms from expensive engineering demos. Click any signal to unpack the investor rationale.

The Closing Thesis

The intelligence layer of every major physical industry is being rebuilt. The question is not whether it will happen — compute economics, national security imperatives, and the climate transition guarantee it. The question is: who builds the platform that becomes the nervous system of physical-world intelligence? The answer will not be found in the model with the best benchmark. It will be found in the company with the deepest physical data flywheel, the broadest certification stack, and the operational integration that makes the AGI Engineer progressively harder to displace with every deployment.

For investors with a 7–10-year horizon and an appetite for category-defining risk, this is precisely the type of infrastructure-level opportunity that generates the outlier return profiles this asset class was designed to capture. The AGI Engineer is not the future of AI. It is the future of engineering — and engineering builds everything.

"The moat is not the model. The moat is the closed loop between intelligence and physical reality — and every hour of deployment deepens it."

About Opulentia Ventures

Opulentia Ventures operates as a “VC Tribe,” consolidating resources from experienced investors to support pioneering companies advancing technology, healthcare, and national security. Headquartered in the Washington, DC, metro area, the firm leverages deep government and defense-sector relationships to identify emerging opportunities at the intersection of innovation and national priorities.